The Mirage of Momentum: March Jobs Report Cements Fed’s 'Higher for Longer' Strategy

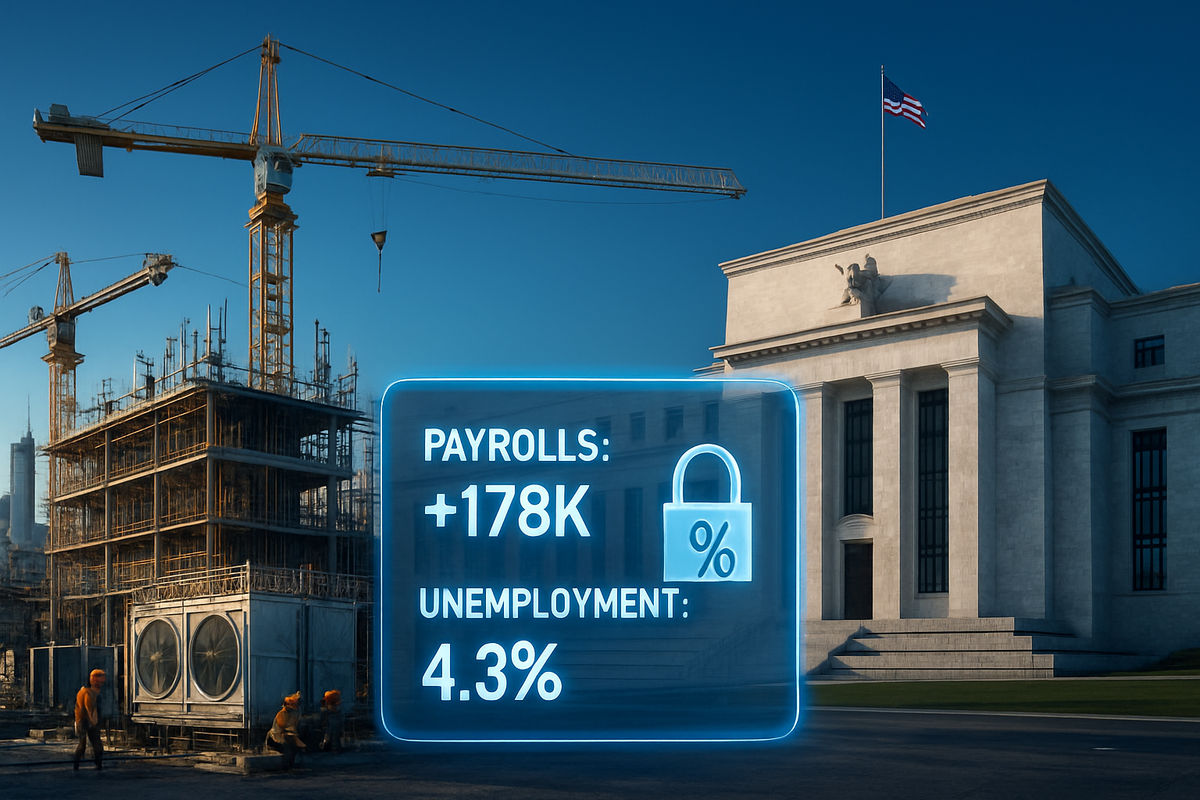

The U.S. labor market staged a defiant, if complicated, comeback in March 2026, adding a surprising 178,000 jobs and pushing the unemployment rate down to 4.3%. For a Federal Reserve currently grappling with a "second wave" of inflation driven by trade tariffs and energy shocks, the data is a clear signal that the economy is not yet cooling enough to warrant the rate cuts markets have been desperate for. The report effectively locks in the Fed’s "higher for longer" stance, as the resilience of the American worker continues to outpace the drag of high borrowing costs.

While the headline numbers suggest a robust expansion, the underlying reality is one of a "low-hire, low-fire" equilibrium. The 178,000 gain represents a sharp reversal from February’s downwardly revised figures, which were hampered by a massive, multi-sector healthcare strike and severe winter storms. However, with the Federal Funds Rate holding steady at 3.50%–3.75%, this "mirage of momentum" provides Federal Reserve Chair Jerome Powell the ammunition he needs to maintain a hawkish pause as he prepares to hand over the reins of the central bank later this year.

Rebounding from the Brink: A Breakdown of the March Surprise

The March employment report arrived at a critical juncture for the U.S. economy. Following a turbulent start to 2026—marked by the "Liberation Day" tariff regime and a significant healthcare strike at Kaiser Permanente—economists had braced for a sluggish 60,000 to 65,000 job gain. Instead, the 178,000 print nearly tripled consensus estimates. Much of this growth was concentrated in the construction and infrastructure sectors, which are currently being fueled by a historic buildout of artificial intelligence data centers across the "Silicon Heartland."

The timeline leading to this report was fraught with volatility. In late 2025, inflation began to "creep" back toward 3% as businesses exhausted their pre-tariff inventories and passed higher costs onto consumers. This was compounded by an energy shock in the Middle East that pushed crude prices upward, complicating the Fed's disinflation path. By the time the March data was collected, the resolution of several major labor disputes provided a "rubber band" effect, with thousands of workers returning to payrolls in the healthcare and transportation sectors.

Initial market reactions were swift and predictably sharp. The 10-year Treasury yield drifted higher toward 4.4% as traders realized that a summer rate cut was effectively off the table. While the unemployment rate fell from 4.4% to 4.3%, analysts were quick to point out that this was partially driven by a decline in labor force participation, which fell to 61.9%. As the U.S. population ages and net immigration continues to slow, the "break-even" rate of job growth required to keep unemployment steady has dropped significantly, making even modest gains like 178,000 feel like a "blockbuster" in the current demographic context.

Corporate Champions and Casualties in the 4.3% Era

For the titans of Wall Street, the "higher for longer" reality is a double-edged sword. JPMorgan Chase (NYSE:JPM) has signaled that it is on track to hit its ambitious 2026 Net Interest Income target of $103 billion, leveraging high-yielding credit card balances and stable deposit costs. Meanwhile, Goldman Sachs (NYSE:GS) is pivoting toward fee-based income, with CEO David Solomon noting that the stable rate environment is finally providing the predictability needed to restart the dormant IPO and M&A markets.

The real winners of the March report, however, are the companies powering the digital backbone of the nation. Nvidia (NASDAQ:NVDA) remains the primary beneficiary of a $500 billion capital expenditure wave from tech hyperscalers. However, the labor report highlights a growing execution risk: a massive shortfall of skilled tradespeople. Vertiv (NYSE:VRT), a specialist in data center cooling, and Equinix (NASDAQ:EQIX) are facing record order backlogs, but their ability to deliver is being tested by the high cost of the very workers the March report highlighted.

Conversely, the retail sector is feeling the squeeze of the "Tariff Shock." Walmart (NYSE:WMT) recently reached a historic $1 trillion market cap but issued a cautious 2026 outlook, warning that general merchandise inflation is tracking over 3% due to import duties. Target (NYSE:TGT) is similarly navigating an administrative nightmare, attempting to reclaim billions in duties following a Supreme Court ruling that challenged the legality of universal tariffs. For these retailers, 4.3% unemployment is a floor for consumer spending, but the rising cost of goods is eating away at the "everyday low price" promise that defines their brands.

The Structural Shift: Why 2026 is Not 2024

The significance of the March report extends far beyond a single month’s data; it represents a fundamental shift in how we define a "healthy" labor market. In the 2020-2024 era, 178,000 jobs would have been considered a standard, if not underwhelming, performance. In 2026, it is a sign of an overheated engine. The "higher for longer" policy is no longer just about cooling demand; it is a structural necessity in an economy where the supply of labor is shrinking due to a "silver tsunami" of retirements and a pivot toward AI automation.

This event also highlights the policy collision course between the Federal Reserve and the current administration. As the Fed tries to quell inflation, the "One Big Beautiful Bill Act" (OBBBA) and its associated tariffs are acting as a pro-inflationary force. This creates a "no landing" scenario where the economy continues to grow, but inflation remains stubbornly above the 2% target. Historical precedents, such as the stagflationary periods of the 1970s, are being studied with renewed vigor as the Fed risks keeping rates high even as the underlying quality of the labor market—specifically for entry-level and knowledge-based roles—begins to soften.

The Road Ahead: Navigating the 'Warsh' Era

Looking forward, the market’s attention now shifts to the May FOMC meeting and the impending leadership change at the Federal Reserve. Jerome Powell’s term expires in May, and the nomination of Kevin Warsh to succeed him suggests a continuation, or even an intensification, of the hawkish "higher for longer" philosophy. Investors should expect a strategic pivot from companies that have relied on "cheap money" strategies, as the era of 3%+ interest rates appears to be a permanent fixture of the late-2020s economy.

In the short term, the housing market remains the most sensitive pressure point. D.R. Horton (NYSE:DHI), the nation’s largest homebuilder, has responded to 7% mortgage rates by "shrinking the American home," focusing on smaller, more efficient floor plans that first-time buyers can still afford. If unemployment remains at 4.3%, a foreclosure wave is unlikely, but the "Great Lock-In"—where homeowners refuse to sell and lose their low 2021-era rates—will continue to limit inventory, keeping home prices artificially high despite the Fed's efforts.

Conclusion: A Delicate Balance in a Volatile World

The March jobs report is a testament to the resilience of the American economy, but it is also a warning. The addition of 178,000 jobs and a 4.3% unemployment rate provides a temporary sense of security, yet the twin threats of tariff-driven inflation and a shrinking labor force loom large. For the Federal Reserve, the data confirms that there is no room for error; cutting rates too early could reignite a wage-price spiral, while holding too long could eventually break the "low-fire" streak that has kept the economy afloat.

As we move toward the second half of 2026, investors should keep a close eye on the transition of power at the Fed and the pass-through effects of the current trade regime. The labor market is the final fortress protecting the economy from a formal recession, but as the quality of that growth shifts toward high-cost infrastructure and away from discretionary consumption, the cracks in the foundation are becoming harder to ignore.

This content is intended for informational purposes only and is not financial advice.