Oil Shocks and Economic Divergence: Previewing a High-Stakes Earnings Week

As the first quarter of 2026 draws to a close, Wall Street is bracing for a tumultuous earnings season that arrives amidst a backdrop of geopolitical upheaval and significant market volatility. With the S&P 500 coming off a 4.6% decline in the first quarter, investors are looking to the opening salvo of corporate reports to determine if the "Oil Shock of 2026" and a cooling labor market will derail the fragile economic expansion. This week marks a critical inflection point as heavyweights in the travel, finance, and consumer staples sectors prepare to open their books, offering the first clear look at how corporate balance sheets are holding up against $110-per-barrel Brent crude.

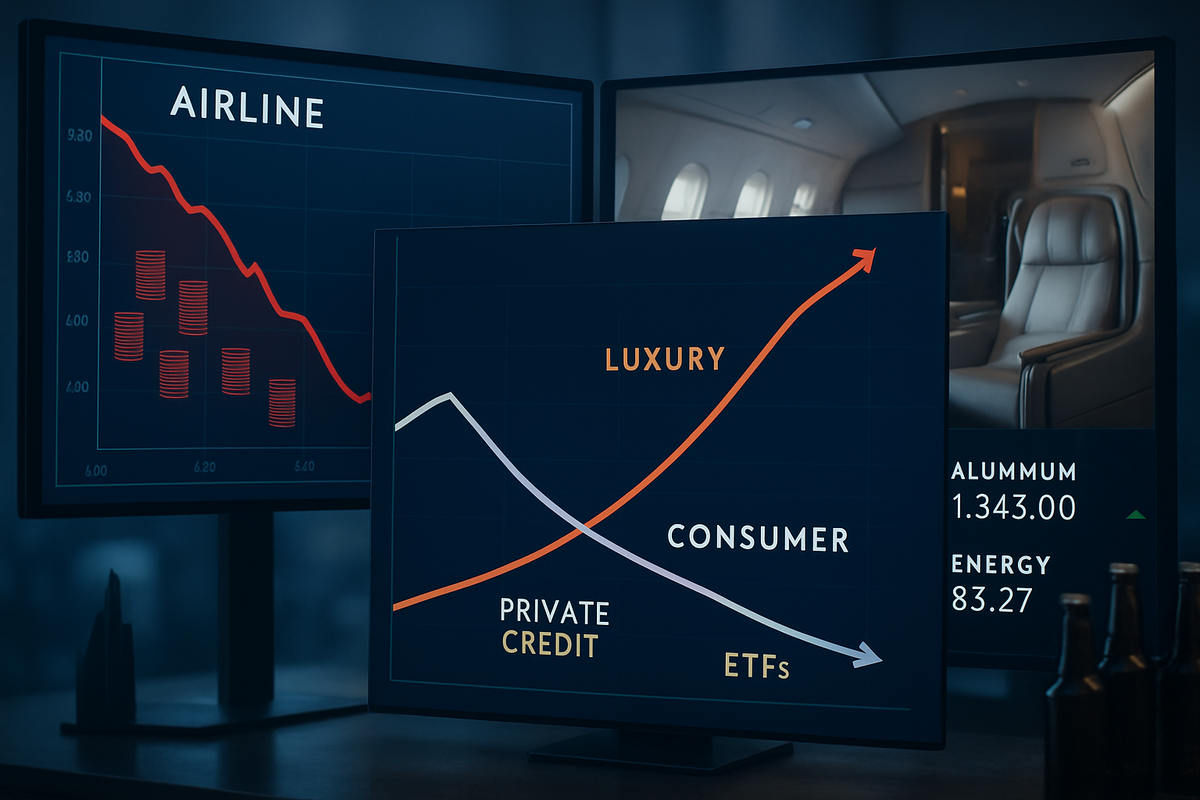

The upcoming reports from Delta Air Lines (NYSE: DAL), BlackRock (NYSE: BLK), and Constellation Brands (NYSE: STZ) are expected to highlight a growing "K-shaped" economic reality. While high-income households continue to spend on premium travel and luxury goods, the broader consumer base is beginning to buckle under the weight of national gas prices that have surged past $4.00 per gallon following recent military escalations in the Middle East. For investors, the focus this week will be less on historical performance and more on forward-looking guidance in a world where the Federal Reserve has been forced to pause its rate-cutting cycle, holding steady at a restrictive 3.50%–3.75%.

Resilience Amid Volatility: The Early Birds of April

The week officially kicks off on Wednesday, April 8, with a double-header from Delta Air Lines and Constellation Brands. Delta is entering the earnings ring at a moment of maximum pressure for the aviation industry. Just three months ago, oil was trading at a manageable $55 per barrel; the subsequent spike to $110 has sent airline fuel models into a tailspin. Analysts have already slashed EPS estimates for Delta by roughly 11% in the last month, now expecting a consensus range of $0.62 to $0.64. Despite these headwinds, the airline is expected to report a revenue increase of nearly 9% year-over-year, driven largely by its dominance in the premium cabin segment and its unique ownership of the Trainer refinery, which may provide a slim margin of protection compared to competitors like United Airlines (NASDAQ: UAL).

Later that same day, Constellation Brands will report what analysts predict could be its lowest quarterly earnings in five years. The company is in the final stages of a painful portfolio cleaning, having divested several lower-end wine and spirits brands to double down on its Mexican beer juggernaut, Modelo Especial. With incoming CEO Nicholas Fink set to take the reins on April 13, investors will be listening intently to the post-market call for his vision of the company’s "beer-first" future. The following Tuesday, April 14, the focus shifts to the capital markets as BlackRock reports. As the world’s largest asset manager, BlackRock's report will be a referendum on the health of private credit markets, which are currently facing their first real test of a full credit cycle following a string of leveraged loan defaults in late 2025.

Winners and Losers in the New Economic Climate

In this environment of high energy costs and stagnant interest rates, the gap between industry leaders and laggards is widening. Delta Air Lines is positioned as a potential winner in the "K-shaped" recovery; by focusing on high-margin international routes and luxury lounges, the carrier is successfully capturing the spend of affluent travelers who remain largely unaffected by rising gas prices. Conversely, low-cost carriers like Southwest Airlines (NYSE: LUV) and JetBlue Airways (NASDAQ: JBLU), which cater to more price-sensitive "main cabin" flyers, are likely to face significant margin compression as their customer base trims discretionary travel to pay for essential heating and commuting costs.

In the beverage space, Constellation Brands’ strategy of "premiumization" will be put to the test. While its Modelo and Pacifico brands continue to dominate the imported beer market, the company faces rising costs from aluminum tariffs, which have jumped as much as 50% since March. This puts them in a precarious position compared to Molson Coors (NYSE: TAP), which may benefit if consumers "trade down" to more affordable domestic lagers. Meanwhile, BlackRock stands to win from the current market volatility as investors flee to the liquidity of its iShares ETF suite, though its private credit holdings remain a point of concern. The company's integration of Global Infrastructure Partners (GIP) is seen as a strategic masterstroke, positioning it to profit from the massive data center buildouts required for the ongoing AI revolution.

Macro Significance: Energy Shocks and the Fed's Dilemma

The broader significance of this earnings week cannot be overstated. We are currently witnessing a "creative destruction" phase of the market, where the AI-driven valuation premiums of 2024 and 2025 are being tested against the cold reality of high capital expenditures and geopolitical risk. The "Oil Shock of 2026" has effectively reignited inflation fears that many thought were buried. This has placed the Federal Reserve in a difficult position: they cannot cut rates to stimulate the flagging economy without risking a secondary inflation spiral driven by energy costs.

This situation echoes the energy crises of the 1970s, though with a modern twist. In 2026, the economy is far more reliant on electricity for AI and EVs, yet still tethered to global oil markets for logistics and travel. The upcoming earnings reports will provide essential data on whether corporations can pass these rising costs onto consumers or if they will have to absorb them, leading to a broader "earnings recession." Furthermore, the regulatory environment is shifting; the recent "One Big Beautiful Bill Act" provided tax relief that has bolstered corporate balance sheets, but investors are beginning to wonder if those gains are being entirely swallowed by rising operational costs.

The Path Ahead: Strategic Pivots and Market Risks

As we look toward the rest of 2026, the primary challenge for these companies will be adaptability. Delta Air Lines may need to accelerate the retirement of its less fuel-efficient aircraft or seek further consolidation to maintain its pricing power. For BlackRock, the focus will likely shift toward "infrastructure as an asset class," moving away from traditional equities and into the tangible assets—power grids, pipelines, and data centers—that are essential in a volatile world. The success of their $12.5 billion GIP acquisition will be the yardstick by which CEO Larry Fink’s final chapters are measured.

For Constellation Brands, the immediate future involves navigating a "wellness" trend that is slowly eroding traditional alcohol consumption volumes. The market will be watching to see if Nicholas Fink pivots the company toward non-alcoholic "social beverages" or further expands their Mexican import dominance. The short-term possibility of a minor recession remains high if oil remains above $100 per barrel for the duration of the summer driving season, suggesting that defensive positioning may be the theme of the quarter.

Closing the Books on Q1

This earnings week serves as a sobering reminder that the "Goldilocks" economy of the mid-2020s has given way to a more fragmented and volatile era. The key takeaways for investors are clear: watch the fuel surcharges, monitor the resilience of the premium consumer, and keep a close eye on the health of private credit markets. While the headline numbers for Delta and Constellation may show the scars of a difficult quarter, the underlying health of their core "power brands" will dictate their trajectory through the end of the year.

Moving forward, the market will likely remain in a "wait-and-see" mode regarding the Iran conflict and its impact on global supply chains. Until there is a clear resolution to the energy spike, volatility will remain the only constant. Investors should prioritize companies with high "moats" and the ability to maintain margins through pricing power, as the divergence between the winners and losers of the 2026 economy continues to sharpen.

This content is intended for informational purposes only and is not financial advice.