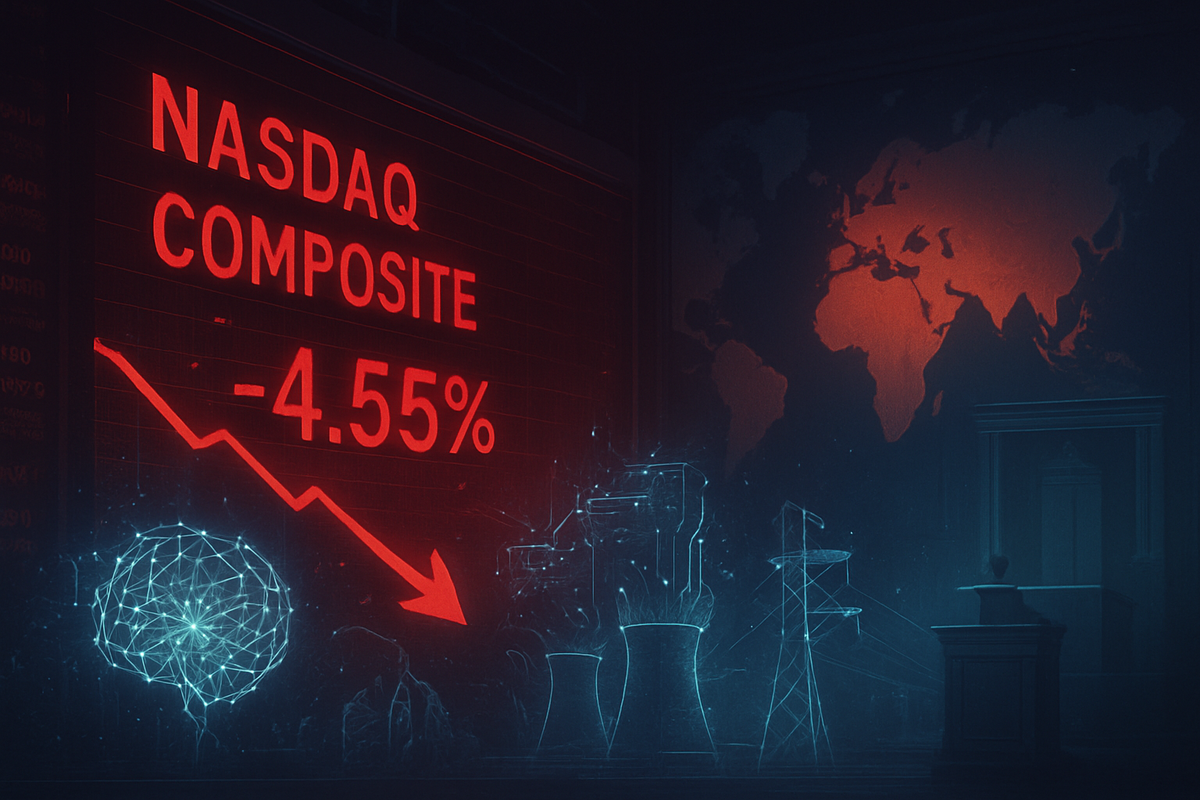

Nasdaq Enters Correction Territory Amid Iranian Conflict and Inflationary Warnings

The tech-heavy Nasdaq Composite has officially entered technical correction territory, marking a swift and sobering reversal for a market that had previously been buoyed by the relentless momentum of the artificial intelligence boom. Between March 26 and March 31, 2026, the index plummeted 10% from its recent all-time highs, as a "perfect storm" of macroeconomic and geopolitical headwinds converged to rattle investor confidence. The decline was punctuated by a frantic sell-off during the final trading sessions of the first quarter, leaving many to wonder if the multi-year AI rally has finally hit a "Power Wall."

The primary catalysts for the downturn include a stark shift in rhetoric from European Central Bank (ECB) President Christine Lagarde regarding persistent inflation and the deepening military conflict in Iran, which has sent global energy markets into a tailspin. As oil prices hover near $120 per barrel, the high-growth valuations of the technology sector have come under intense scrutiny, with traders pivoting away from speculative AI bets in favor of more defensive, "real economy" assets.

A Week of Turmoil: The March Sell-Off Timeline

The slide began in earnest on March 26, following a series of hawkish remarks from ECB President Christine Lagarde. Speaking at a high-level summit in Frankfurt, Lagarde warned that the "disinflationary dream" of 2025 had been shattered by the soaring costs of energy and logistics. She signaled that the ECB is prepared to "forcefully" hike interest rates again in the second quarter of 2026 if the headline inflation rate, currently projected to hit 2.6%, does not stabilize. This caught the markets off-guard, as most analysts had expected a period of stability or even further cuts.

Compounding the anxiety is the escalating war in Iran, which entered a dangerous new phase in late March. "Operation Epic Fury," the joint military campaign led by the United States and Israel, has successfully targeted Iranian missile infrastructure but has also led to a near-total blockade of the Strait of Hormuz. As one of the world's most vital maritime oil chokepoints remains closed, the threat of a global energy crisis has become the central focus of Wall Street. For the Nasdaq, which is highly sensitive to the cost of capital and discretionary spending, the prospect of prolonged high inflation and high interest rates has triggered a mass exodus.

The reaction from the industry has been one of defensive positioning. By the afternoon of March 30, the "Magnificent Seven" and other AI leaders saw their gains from the previous six months evaporated in just four trading sessions. Market volatility, as measured by the VIX, surged to its highest level since the early stages of the regional banking crisis of years past, reflecting a fundamental shift from "FOMO" (fear of missing out) to a desperate search for liquidity.

The AI "Power Wall": Winners and Losers in a Shifting Landscape

The most significant casualties of this correction have been the semiconductor and hardware giants that led the 2024-2025 rally. Nvidia (NASDAQ:NVDA) and ASML (NASDAQ:ASML) have seen their shares drop significantly as the market transitions from "chip demand" to "implementation fatigue." Investors are increasingly concerned that the massive capital expenditures by firms like Microsoft (NASDAQ:MSFT) and Alphabet (NASDAQ:GOOGL) have yet to yield the hyper-growth in revenue required to justify current P/E multiples, especially as the "Power Wall"—the physical limit of electricity availability to run massive data centers—begins to stifle expansion.

Conversely, the defense and energy sectors have emerged as the primary beneficiaries of the current chaos. Lockheed Martin (NYSE:LMT) and Raytheon (NYSE:RTX) have seen a surge in interest as the conflict in Iran necessitates an increase in military hardware and advanced missile defense systems. Furthermore, the "Great Rotation" has seen capital flow into utility providers and nuclear energy companies that are seen as essential for the long-term viability of the AI infrastructure.

While tech titans like Meta (NASDAQ:META) and Amazon (NASDAQ:AMZN) have the cash reserves to weather a downturn, smaller AI startups that rely on cheap credit are facing an existential crisis. The rising cost of energy is not just a consumer problem; it is a direct overhead cost for every data center operator in the world. As these costs are passed down the chain, the "AI gold rush" is being replaced by a more disciplined, and perhaps painful, era of fiscal pragmatism.

Breaking the AI Fever: Broader Market Implications

The current correction is not merely a localized event but fits into a broader global trend of "geopolitical inflation." For years, the market assumed that the deflationary nature of technology would keep prices low, but the 2026 energy shock has proven that even the most advanced AI models cannot run without affordable power and stable supply chains. This event draws eerie comparisons to the 2022 energy crisis following the invasion of Ukraine, but with the added complexity of a much larger and more interconnected tech ecosystem.

Regulatory and policy implications are also looming. The "One Big Beautiful Bill Act" (OBBBA) of 2025, which was designed to bolster domestic tech manufacturing, is now being criticized by some lawmakers as inflationary. If the war in Iran persists, there is growing pressure on the U.S. and European governments to implement energy subsidies or price controls, which could lead to further market distortions. The historical precedent of the 1970s oil shocks serves as a haunting reminder that stagflation—stagnant growth combined with high inflation—is a very real risk when energy and geopolitics collide.

Furthermore, the Nasdaq's fall has ripple effects across global indices. The tech-heavy KOSPI in South Korea and the Nikkei 225 in Japan have also faced downward pressure, as the global supply chain for high-end electronics is inextricably linked to the stability of both the Middle East and the Western consumer’s wallet.

The Road Ahead: Pivot or Perish?

In the short term, investors should prepare for continued volatility as the first-quarter earnings season approaches. The focus will shift from "AI potential" to "AI profitability." Companies that cannot demonstrate a clear path to monetization in a high-cost environment may see their valuations slashed further. We may also see strategic pivots; many tech firms are already exploring investments in small modular reactors (SMRs) and other off-grid energy solutions to bypass the "Power Wall" that is currently capping their growth.

Longer-term, the Nasdaq correction might actually serve as a healthy "reset" for a market that had become dangerously top-heavy. If the Iran conflict can be contained and the ECB manages a "managed landing" rather than a hard crash, the current entry points for tech stocks could eventually be seen as a generational buying opportunity. However, that scenario depends entirely on a de-escalation of regional hostilities—a prospect that remains uncertain as of the end of March.

Market Wrap-Up and Investor Outlook

The final days of March 2026 will be remembered as the moment the AI-fueled bull market met its toughest adversary: reality. The combination of ECB hawkishness and the fog of war in Iran has reminded investors that no sector, no matter how revolutionary, is immune to the laws of macroeconomics. The Nasdaq's 10% slide into correction territory is a clear signal that the era of "easy money" and unbridled optimism has ended, replaced by a more cautious and calculating market environment.

Moving forward, the key metrics to watch will be the price of Brent Crude and the ECB's next policy meeting in April. If inflation expectations continue to unanchor, the "correction" could easily transition into a full-blown bear market. Investors should remain vigilant, focusing on companies with strong balance sheets, pricing power, and a clear strategy for navigating the ongoing energy transition.

The coming months will determine whether this is a temporary pause in a larger secular bull market or the beginning of a prolonged downturn that will reshape the technological and financial landscape for years to come.

This content is intended for informational purposes only and is not financial advice.