Fed Cuts Key Interest Rate to 3.75%-4.00% Amidst Persistent Inflation and Weakening Labor Market

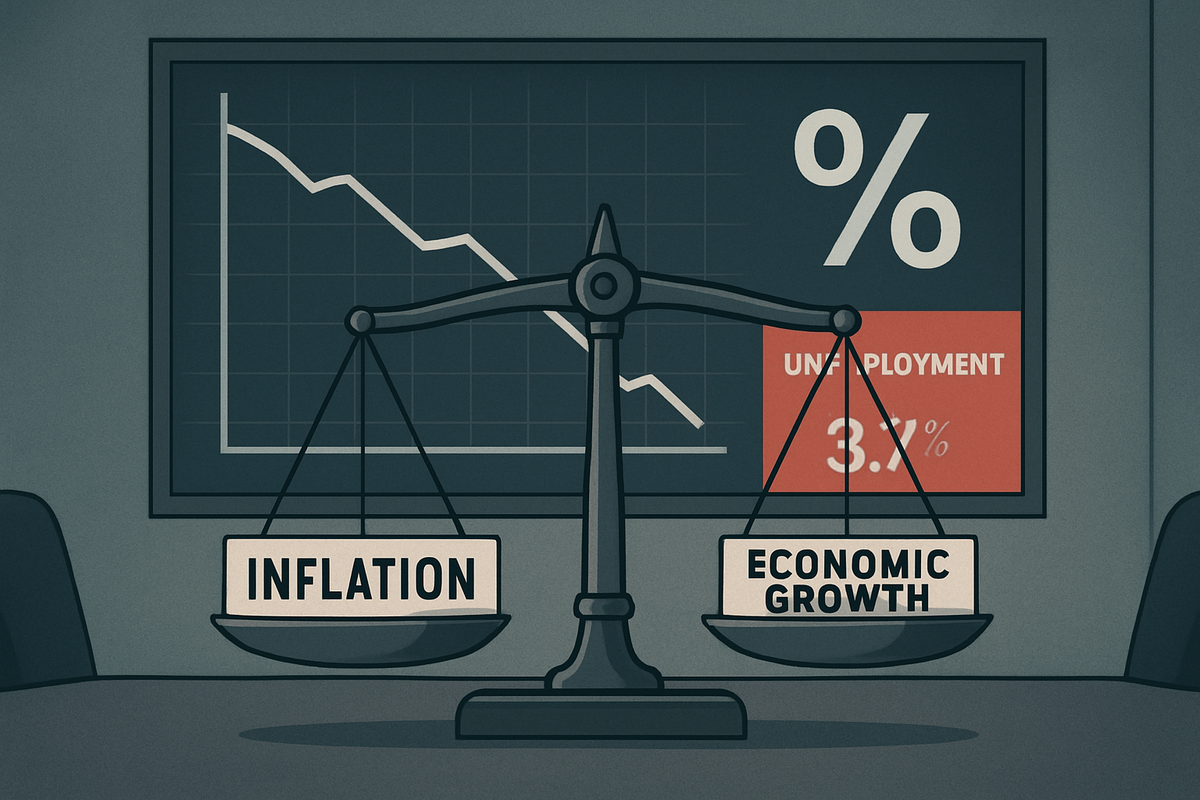

In a closely watched decision, the Federal Open Market Committee (FOMC) of the U.S. Federal Reserve today, October 29, 2025, announced a cut to its benchmark interest rate, lowering the target range by 25 basis points to 3.75%-4.00%. This move marks the second rate reduction by the central bank this year, signaling a strategic pivot aimed at bolstering a softening economy despite ongoing inflation concerns. The decision reflects a delicate balancing act by the Fed, attempting to stimulate growth and a weakening labor market without reigniting price pressures that have proven stubbornly persistent.

The immediate implications of this rate cut are significant. Lower borrowing costs are expected to provide a much-needed impetus to consumer spending and business investment, potentially offering relief to sectors sensitive to interest rates such as housing and automotive. However, the backdrop of a Consumer Price Index (CPI) stubbornly at 3% – above the Fed's 2% target – underscores the challenge. This cut suggests the Fed is prioritizing economic stabilization and employment over an aggressive inflation fight, at least for the time being, a stance that will be scrutinized by markets and economists alike.

FOMC Navigates Economic Headwinds with Second Rate Cut

The Federal Reserve's decision to trim the federal funds rate to 3.75%-4.00% was made amidst a complex economic landscape. The previous target range stood at 4.00%-4.25%. This move follows a similar rate cut in September, indicating a proactive approach by the central bank to address emerging economic vulnerabilities. While inflation, as measured by the CPI, registered 3% for the 12 months ending September 2025 (a slight uptick from August's 2.9%), the FOMC's statement highlighted growing concerns over the labor market.

Leading up to this decision, economic data had painted a picture of slowing momentum. Job gains had moderated throughout 2025, and the unemployment rate, though still historically low, had begun to tick upwards. Most notably, private-sector payrolls reportedly contracted in September, a stark indicator of weakening labor demand. This deterioration in the employment picture appears to have swayed the committee, prompting them to lean towards accommodative monetary policy despite inflation remaining above their long-term target.

Key players involved in this decision include Fed Chair Jerome Powell, who emphasized the committee's focus on the "balance of risks" in the U.S. economy. While the rate cut was largely anticipated by market participants, there was internal disagreement among FOMC members regarding the appropriate path forward. Some members reportedly advocated for larger cuts, while others preferred to hold rates steady, underscoring the divergent views on how best to navigate the current economic challenges. The ongoing U.S. government shutdown further complicated matters, delaying the release of critical economic data and adding to the uncertainty surrounding the Fed's outlook.

Initial market reactions were somewhat subdued, as the cut was largely priced in. However, the bond market saw some movement, with shorter-term Treasury yields generally declining, reflecting expectations of continued lower rates. The stock market's reaction was mixed, with some sectors benefiting from the prospect of cheaper borrowing, while others remained cautious due to underlying economic concerns. The U.S. dollar experienced slight depreciation against major currencies, a typical response to interest rate reductions, as it makes dollar-denominated assets less attractive to foreign investors.

Corporate Winners and Losers in a Lower Rate Environment

The Federal Reserve's decision to cut interest rates will undoubtedly create a ripple effect across various industries, creating clear winners and losers in the corporate landscape. Companies with significant debt loads or those heavily reliant on consumer financing are poised to benefit substantially from reduced borrowing costs.

Potential Winners:

- Housing and Real Estate: Homebuilders like D.R. Horton (NYSE: DHI) and Lennar Corp. (NYSE: LEN), along with real estate investment trusts (REITs) such as Simon Property Group (NYSE: SPG), could see increased demand as mortgage rates decline, making homeownership and property development more affordable. This could stimulate sales and investment in the sector.

- Automotive Industry: Manufacturers like General Motors (NYSE: GM) and Ford Motor Company (NYSE: F) often rely on consumer financing for vehicle purchases. Lower interest rates could lead to more affordable car loans, boosting sales volumes and potentially improving profit margins.

- Consumer Discretionary: Companies in retail and other consumer discretionary sectors, such as Amazon (NASDAQ: AMZN) and Starbucks (NYSE: SBUX), may experience an uptick in consumer spending as individuals have more disposable income due to lower debt service costs and increased confidence.

- Growth-Oriented Tech Companies: Technology companies, especially those that are still in growth phases and require significant capital investment, often benefit from lower interest rates as it reduces the cost of financing their expansion. Companies like NVIDIA (NASDAQ: NVDA) or Tesla (NASDAQ: TSLA) might find it cheaper to fund R&D or new projects.

- Highly Leveraged Companies: Any company with substantial variable-rate debt will see an immediate reduction in interest expenses, leading to improved profitability.

Potential Losers:

- Banks and Financial Institutions: While lower rates can stimulate lending, a narrower net interest margin (NIM) – the difference between what banks earn on loans and pay on deposits – can put pressure on profitability for banks like JPMorgan Chase (NYSE: JPM) and Bank of America (NYSE: BAC). Their ability to generate revenue from lending might be constrained if deposit rates don't fall as quickly as lending rates.

- Insurance Companies: Insurers often hold large portfolios of fixed-income securities. Lower interest rates can reduce the returns on these investments, impacting their overall profitability and ability to meet long-term liabilities.

- Seniors and Savers: Individuals relying on fixed-income investments, such as savings accounts, certificates of deposit (CDs), and money market funds, will see diminished returns on their savings, impacting their income and purchasing power.

- Companies with Strong Cash Positions: While not necessarily "losers," companies sitting on large cash reserves, like Apple (NASDAQ: AAPL) or Microsoft (NASDAQ: MSFT), may see a slight reduction in the interest income generated from those reserves.

The impact will largely depend on each company's capital structure, customer base, and sensitivity to interest rate fluctuations. Companies that can effectively leverage the lower cost of capital for strategic investments or to reduce existing debt will be best positioned to thrive in this new environment.

Broader Economic and Regulatory Implications

The Federal Reserve's decision to cut interest rates is not an isolated event but rather a significant move within a broader economic context, carrying wide-ranging implications for industry trends, regulatory frameworks, and international financial dynamics. This shift signals a departure from the previous tightening cycle, indicating that the Fed perceives the risks to economic growth as outweighing the immediate concerns of elevated inflation.

This rate cut fits into a broader global trend where several central banks are contemplating or have already implemented easing measures to counter economic slowdowns. It reflects a growing recognition among policymakers that the post-pandemic recovery is facing new headwinds, including persistent supply chain issues, geopolitical tensions, and a general cooling of global demand. For instance, if other major economies like the European Union or Japan maintain or further ease their monetary policies, the Fed's move could be seen as aligning with a global trend of economic accommodation.

The potential ripple effects on competitors and partners are substantial. For export-oriented U.S. companies, a weaker dollar—a common outcome of rate cuts—could make their goods and services more competitive on the international market. This might benefit large multinational corporations like Coca-Cola (NYSE: KO) or Boeing (NYSE: BA). Conversely, companies heavily reliant on imports might face higher costs if the dollar weakens significantly. In the financial sector, banks with international operations might see shifts in capital flows as investors seek higher yields elsewhere, impacting their foreign exchange and lending activities.

From a regulatory and policy perspective, this rate cut could invite increased scrutiny from Congress, particularly regarding the Fed's dual mandate of maximum employment and price stability. If inflation remains sticky despite the rate cut, or if the labor market continues to weaken, the Fed's independence and decision-making process could come under political pressure. There might also be renewed calls for fiscal stimulus to complement monetary policy, especially if the government shutdown persists and further impedes economic activity. This could lead to debates over infrastructure spending, tax policies, or targeted aid programs.

Historically, periods of rate cuts following a tightening cycle often occur when the economy is either entering a recession or experiencing a significant slowdown. Comparisons can be drawn to periods like the early 2000s or 2007-2008, where the Fed aggressively cut rates to stave off or mitigate economic crises. However, a key difference in the current environment is the persistent, albeit moderate, inflation. This makes the Fed's balancing act particularly challenging, as it must avoid the perception of being behind the curve on either inflation or economic contraction. The current scenario is less about a full-blown crisis and more about proactive risk management in an uncertain global economy.

The Path Forward: Navigating Uncertainty

The FOMC's recent rate cut sets the stage for a period of heightened observation and potential volatility in the financial markets. In the short term, the market will be keenly watching incoming economic data, particularly inflation reports and employment figures, to gauge the effectiveness of the Fed's policy adjustment. Any signs of inflation re-accelerating could prompt the Fed to pause or even reverse its easing stance, while continued labor market weakness might necessitate further rate cuts. The ongoing U.S. government shutdown adds a layer of uncertainty, as delays in data releases could obscure the true state of the economy, making the Fed's decision-making process even more challenging.

In the long term, this rate cut could be the precursor to a more sustained period of lower interest rates, particularly if global economic growth remains subdued. This scenario would require companies to adapt their capital allocation strategies, potentially favoring investments in long-duration assets and projects with lower hurdle rates. Strategic pivots might include a renewed focus on debt refinancing for businesses to lock in lower rates, or a shift in investment portfolios towards growth stocks that tend to perform well in lower-rate environments.

Market opportunities could emerge in sectors that are highly sensitive to interest rates, such as real estate, utilities, and certain segments of the technology industry. Investors might also look for opportunities in emerging markets, where a weaker dollar could boost returns. Conversely, challenges may arise for financial institutions grappling with narrower net interest margins and for savers who face diminished returns on traditional savings instruments.

Several potential scenarios could unfold. In an optimistic scenario, the rate cut successfully stimulates economic activity, leading to a soft landing where inflation gradually moderates without a significant increase in unemployment. In a more pessimistic scenario, the rate cut proves insufficient to counter economic headwinds, leading to a prolonged period of slow growth or even a mild recession, while inflation remains elevated—a stagflationary environment. Another scenario involves the Fed needing to reverse course quickly if inflation unexpectedly surges, potentially leading to market instability. Investors should closely monitor the Fed's forward guidance, statements from FOMC members, and the geopolitical landscape, which continues to pose risks to global supply chains and energy prices.

A Pivotal Moment for the Economy

The Federal Reserve's decision to cut the key interest rate to 3.75%-4.00% marks a pivotal moment in the current economic cycle, reflecting a strategic shift to prioritize economic growth and a stable labor market amidst persistent, albeit moderate, inflation. The central bank is navigating a complex environment, attempting to thread the needle between stimulating a slowing economy and preventing an uncontrollable surge in prices. This move signals a more accommodative monetary policy stance, responding to tangible signs of weakening employment and broader economic deceleration.

Moving forward, the market will be closely assessing how this rate cut impacts key economic indicators. Investors should pay particular attention to inflation data, specifically the Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) price index, to see if price pressures begin to ease. Equally crucial will be labor market reports, including unemployment rates and job creation figures, to determine if the Fed's actions are effectively shoring up employment. Corporate earnings reports will also provide valuable insights into how different sectors are adapting to the new interest rate environment and the broader economic conditions.

The lasting impact of this decision will hinge on its ability to foster sustainable economic growth without reigniting inflationary spirals. If successful, it could pave the way for a more stable and robust recovery. However, if inflation remains stubbornly high or if economic growth fails to materialize, the Fed may face difficult choices, potentially leading to further policy adjustments or a reevaluation of its strategy. For investors, the coming months will require vigilance and a nuanced understanding of economic data, as the market navigates the delicate balance between growth, inflation, and the Fed's evolving monetary policy.

This content is intended for informational purposes only and is not financial advice